Stablecoin Regulation 2026: A Global Guide for Businesses in Calgary, New York, and Berlin

- jzanglaw

- Apr 24

- 12 min read

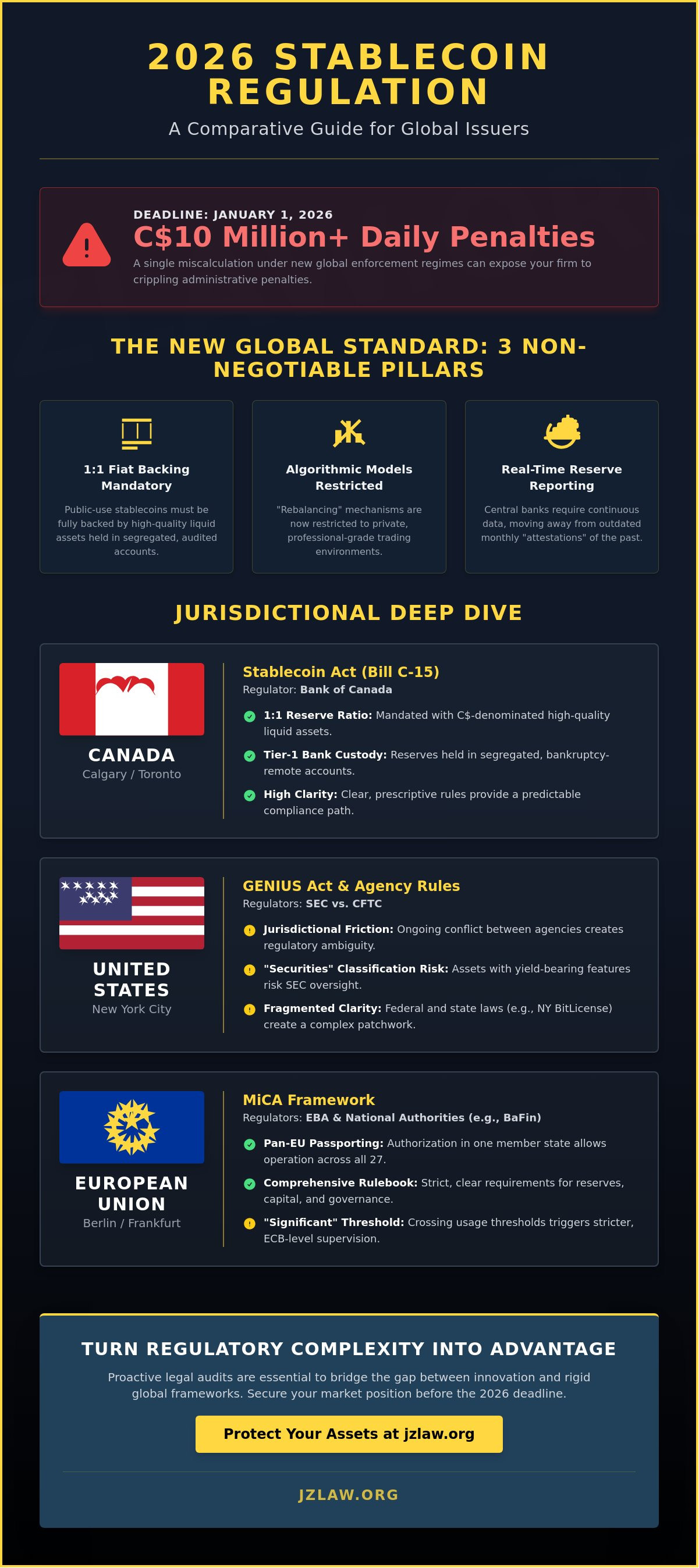

By January 1, 2026, a single miscalculation regarding the "significant stablecoin" threshold could expose your firm to daily administrative penalties exceeding C$10 million under the new global enforcement regime. It’s a reality that fintech leaders in Calgary and New York are currently facing as they grapple with the diverging requirements of the US GENIUS Act and the European Union’s MiCA. You likely recognize that stablecoin regulation is no longer a localized concern but a fragmented, multijurisdictional puzzle that threatens to stall institutional adoption if handled without absolute precision.

We'll provide the strategic clarity you need to navigate the intersection of Canada’s Stablecoin Act and international mandates with professional rigor. This guide identifies specific registration triggers for 2026 in Calgary, New York City, and Berlin, ensuring your compliance strategy remains proactive rather than reactive. We'll examine the Bank of Canada’s latest registration protocols and outline a framework to protect your assets from retroactive enforcement by the SEC or BaFin, turning regulatory complexity into a sustainable competitive advantage.

Key Takeaways

Gain a comprehensive understanding of the 2026 legal standards that define the issuance and reserve management of fiat-backed digital assets.

Compare the jurisdictional nuances of stablecoin regulation across Canada, the US, and the EU to mitigate risks for Calgary-based issuers.

Identify the core compliance requirements for reserve transparency and bankruptcy-remote custody to protect corporate assets and client funds.

Address the complexities of jurisdictional friction and tax liability when scaling fintech operations between Canadian and European markets.

Discover how strategic legal audits can bridge the gap between innovative product development and rigid global regulatory frameworks.

Table of Contents What is Stablecoin Regulation in 2026? Defining the New Standards The 2026 Global Regulatory Map: Canada, USA, and the EU Core Compliance Pillars for Stablecoin Issuers Navigating Jurisdictional Friction in Global Business Hubs Strategic Implementation: How JZ Law Secures Your Market Position

What is Stablecoin Regulation in 2026? Defining the New Standards

By early 2026, stablecoin regulation has evolved from a series of reactionary guidelines into a rigid, global legal architecture. This framework governs the issuance, reserve management, and redemption of digital assets pegged to sovereign currencies. The transition marks the definitive end of the "Wild West" era, characterized by the collapse of unbacked protocols in 2022. Today, the 2026 standards prioritize institutional stability and consumer protection above all else. Before assessing these risks, one must revisit the foundational question: What is a Stablecoin? and why does its specific structure trigger such intense oversight?

For enterprises operating in Calgary, Toronto, or New York, these rules dictate the terms of market entry. Compliance isn't just a legal hurdle; it's the only way to access traditional banking rails and attract institutional capital. In the current landscape, the distinction between "payment stablecoins" and assets treated as securities has been clarified by 2026 case law. If an asset is marketed for its potential yield or managed by a centralized entity that promises profit through secondary market activity, it falls under securities law. Conversely, payment stablecoins must function like digital cash, requiring 100% liquidity and immediate redeemability.

Fiat-Backed vs. Algorithmic: The Legal Divide

The legal environment in 2026 doesn't tolerate the volatility of the 2022 era. Laws such as the US GENIUS Act and the European MiCA framework effectively mandate a 1:1 fiat backing for any token used by the public. Algorithmic models that rely on "rebalancing" mechanisms are now restricted to private, professional-grade trading environments. Under new consumer protection statutes, a "de-pegging" event that lasts longer than 24 hours triggers automatic regulatory intervention and potential criminal liability for directors. A fiat-backed stablecoin is defined under the 2026 Canadian framework as a digital asset that maintains a stable value relative to the Canadian dollar through high-quality liquid assets held in segregated, audited accounts.

The Role of Central Banks in Stablecoin Oversight

The Bank of Canada now exercises direct supervision over retail payment activities involving digital currencies to ensure they don't threaten national financial stability. This oversight is mirrored globally, as the Federal Reserve and Germany's BaFin coordinate on cross-border liquidity standards to prevent contagion. These agencies require real-time reporting of reserve balances, moving away from the monthly "attestations" of the past. JZ Law emphasizes a preventive compliance strategy to avoid the disruption of a central bank audit. By establishing robust internal controls before a regulator knocks, businesses protect their operational continuity and maintain their reputation in an increasingly scrutinized market.

The 2026 Global Regulatory Map: Canada, USA, and the EU

By 2026, the landscape of stablecoin regulation has shifted from fragmented guidelines to rigid, enforceable statutes. A business operating in Calgary faces a different compliance burden than one in New York or Berlin. While the industry once hoped for a global standard, we now see three distinct pillars. There's no "global passport" for stablecoins. Holding a license in Vancouver doesn't grant you the right to operate in Denver or Frankfurt. Regulators in Toronto and Berlin now engage in daily automated data sharing to track cross-border flows; this makes regulatory arbitrage nearly impossible. Issuers must prepare for a world where jurisdictional nuances dictate the cost of capital and the speed of market entry.

Canada’s Stablecoin Act (Bill C-15) and Retail Payments

The enactment of Bill C-15 in early 2025 transformed the Canadian market. Every issuer must now register with the Bank of Canada as a retail payment service provider. This legislation mandates a 1:1 reserve ratio, ensuring redemption at par is a statutory right for every holder. For a Calgary-based fintech, this means maintaining high-quality liquid assets, often denominated in C$, held in segregated accounts at Canadian Tier-1 banks. This framework is a core component of the broader Cryptocurrency Law 2026 standards that govern digital finance. Failure to meet these liquidity requirements results in immediate suspension of the issuer's registration under the Retail Payment Activities Act.

The US GENIUS Act and SEC vs. CFTC Clarity

The 2025 GENIUS Act finally ended the jurisdictional tug-of-war between the SEC and CFTC. It classifies payment stablecoins as a unique category of digital assets rather than traditional securities. However, New York-based companies must still navigate the state's rigorous BitLicense requirements alongside federal mandates. The US Regulatory Framework established by the Treasury Department emphasizes that non-bank issuers must meet bank-like capital standards. This shift has forced many New York platforms to restructure their securities regulation compliance strategies to accommodate tokenized treasury bills and other reserve assets.

MiCA in Berlin and Frankfurt: The EU Standard

In Germany, the Markets in Crypto Assets (MiCA) regulation is now fully operational. Berlin-based issuers are categorized by their scale; those labeled as "Significant Asset-Referenced Tokens" (ARTs) face direct supervision by the European Banking Authority. Capital adequacy requirements are strict, often requiring reserves equal to 2% of the average amount of reserve assets. JZ Law helps Canadian firms bridge the gap when expanding into Berlin, ensuring that domestic compliance translates effectively into the EU’s rigid technical standards. For companies seeking to minimize risk, consulting with a strategic partner early in the expansion phase prevents costly enforcement actions. We provide the precision necessary to navigate these overlapping global requirements without compromising operational efficiency.

Core Compliance Pillars for Stablecoin Issuers

The 2026 regulatory landscape demands a shift from voluntary transparency to rigorous, state-mandated oversight. Issuers operating in Calgary, New York, or Berlin must treat compliance as a core operational function rather than a secondary legal concern. The primary objective of modern stablecoin regulation is to eliminate the systemic risks that led to historical market de-pegging events. This requires four fundamental pillars: monthly independent third-party audits for reserve transparency, bankruptcy-remote segregation of client funds, strict AML/KYC protocols compliant with FINTRAC's "Travel Rule," and advanced data security measures designed to withstand quantum threats.

Reserve Management and Liquidity Requirements

Issuers must maintain a 1:1 reserve ratio using highly liquid, low-risk assets. Permissible instruments are restricted to Canadian cash (C$), Government of Canada T-bills, or equivalent high-quality liquid assets. The 2026 frameworks strictly prohibit "re-hypothecation," meaning issuers cannot lend or leverage reserve assets to generate additional yield. This preventive measure ensures that liquidity remains available even during extreme market volatility. For firms navigating the complexities of reserve structuring, our team provides specialized guidance on corporate transactions involving stablecoin reserves. These standards align closely with the EU's MiCA Regulation, which has set a global benchmark for asset-referenced tokens and e-money tokens across the European market.

Redemption Rights and Consumer Protection

Consumer protection in 2026 centers on the absolute right to redeem stablecoins for fiat currency at par value. The "T+2" standard has become the global legal expectation, requiring issuers to process redemption requests within two business days. If an issuer faces insolvency, legal frameworks now ensure that segregated client funds are protected from general creditors. Under the 2026 Canadian framework, issuers are legally mandated to maintain a dedicated redemption portal that operates independently of secondary market exchange liquidity. This level of stablecoin regulation builds the long-term trust necessary for institutional adoption. It's a strategic necessity for businesses to implement these protocols before regulatory enforcement actions occur. Our approach focuses on establishing these safeguards early to ensure business continuity and protect the interests of all stakeholders.

Data security protocols have also evolved. By 2026, issuers must demonstrate "quantum-readiness" in their ledger architecture. This involves implementing cryptographic standards that can resist the processing power of emerging quantum computers. Cyber resilience is no longer a best practice; it's a licensing requirement for any entity acting as a money services business in Canada.

Navigating Jurisdictional Friction in Global Business Hubs

Operating a digital asset firm across Calgary, New York, and Berlin creates a triangle of conflicting mandates. By 2026, the divergence in stablecoin regulation between these hubs requires more than just compliance; it demands a proactive legal architecture. Calgary businesses often face the dual pressure of Alberta’s Innovation Act and federal FINTRAC requirements, while their Berlin counterparts must adhere to the finalized MiCA frameworks. Discrepancies in capital reserve ratios or mandatory audit frequencies can paralyze a firm that hasn't synchronized its internal policies across these regions.

Tax structuring presents the most immediate hurdle. Stablecoin issuance in Canada triggers specific corporate tax liabilities that differ significantly from Germany's treatment of digital assets. While Germany might offer exemptions for long-term holdings under certain conditions, the Canadian Revenue Agency (CRA) maintains a rigorous stance on business income derived from crypto transactions. Attempting regulatory arbitrage by migrating to a "light-touch" jurisdiction often backfires. If your entity avoids the oversight of the New York Department of Financial Services (NYDFS), you'll likely find yourself blocked from the Toronto and New York capital markets. This loss of access to institutional liquidity providers who require strict stablecoin regulation adherence can be fatal for growth.

Corporate Structuring for Multijurisdictional Crypto Firms

Success starts with the right foundation. JZ Law provides specialized tax structuring for digital asset companies looking to bridge these gaps. Choosing between Vancouver and Denver as a North American headquarters isn't just about geography. It's a choice between two distinct legal climates regarding enforcement and reporting. Additionally, firms employing remote developers in Berlin must account for "Permanent Establishment" risks. Under German law, a single lead developer with decision-making power can inadvertently create a taxable presence for the entire Canadian corporation, leading to double taxation and administrative penalties.

When Stablecoins Meet Securities Law

Determining if a yield-bearing stablecoin is a security remains a critical pivot point for 2026 offerings. If your protocol distributes rewards to holders, the Ontario Securities Commission (OSC) and the SEC will likely classify it as an investment contract. This classification necessitates a formal Prospectus, a document that's become the gold standard for transparency in the post-2025 market. For firms seeking traditional exits, this level of compliance is a prerequisite for taking companies public through RTOs or traditional IPOs. A centralized legal strategy ensures that decentralized protocols don't crumble under the weight of fragmented global enforcement.

Strategic growth requires a partner who understands the nuance of cross-border compliance. Consult with JZ Law to secure your firm’s regulatory standing in 2026.

Strategic Implementation: How JZ Law Secures Your Market Position

JZ Law serves as the essential conduit between high-speed fintech innovation and the increasingly rigid regulatory frameworks of 2026. As the grace periods for major international frameworks expire, businesses require more than just a list of rules; they need a structural integration of compliance into their daily operations. We facilitate this transition by converting complex legal requirements into actionable business logic, ensuring your venture remains agile while staying strictly within the law.

Our preventive legal audits act as a critical diagnostic tool for firms operating in the digital asset space. We identify compliance gaps before they evolve into costly enforcement actions by bodies like the Canadian Securities Administrators (CSA) or FINTRAC. By the start of 2026, the cost of non-compliance is expected to rise as regulators shift from educational outreach to active litigation. JZ Law mitigates this risk through rigorous stress-testing of your internal protocols.

Strategic corporate transactions in the crypto sector now require a layer of specialized due diligence that traditional firms often overlook. Whether you are pursuing a merger, an acquisition, or a C$10 million financing round, our team ensures that every contract and asset transfer aligns with 2026 crypto laws. John Zang’s specialized focus on niche industries, particularly his work in oil and gas, offers a unique advantage for the development of resource-backed tokens. This intersection of energy sector expertise and blockchain law provides a sophisticated perspective on how physical commodities can be effectively and legally tokenized in global energy hubs like Calgary and Denver.

Customized Compliance Roadmaps

We develop tailored legal strategies that synchronize the specific, often conflicting, regulations of Calgary, Toronto, and Berlin. This multi-jurisdictional approach is vital for firms that move liquidity across borders. Our ongoing advisory services keep your board informed on the latest FINTRAC and SEC guidelines, ensuring that your stablecoin regulation strategy remains current as 2026 progresses. We prioritize the construction of logically closed legal frameworks that eliminate interpretive ambiguity and ensure every operational facet remains within the bounds of statutory requirements.

The JZ Law Advantage: Strategic Partner, Not Just Counsel

JZ Law moves beyond the delivery of dry legal facts to provide business-centric strategic advice that supports your growth. We don't just tell you what the law is; we show you how to use it to gain a competitive edge. To initiate a consultation regarding stablecoin licensing or to restructure your corporate entity for the 2026 landscape, contact our office for a detailed assessment.

Review of jurisdictional licensing requirements for Canada and the EU.

Structural analysis of reserve management protocols.

Drafting of "logically closed" smart contract legal wrappers.

Strategic advisory for cross-border M&A in the fintech sector.

The window for proactive adjustment is closing. Secure your 2026 stablecoin strategy with JZ Law to ensure your business remains resilient in a tightening global market.

Securing Your Market Position in the 2026 Digital Asset Economy

The transition to the 2026 global standards requires a sophisticated understanding of how stablecoin regulation intersects with local mandates from FINTRAC in Canada and the SEC in the United States. Success for businesses in Calgary, New York, and Berlin depends on harmonizing these complex frameworks to prevent operational delays during high-stakes corporate transactions. Our strategic presence in these key financial hubs allows us to provide the precise, preventive counsel necessary to navigate jurisdictional friction effectively. We prioritize your security by ensuring every protocol meets the latest transparency and reserve requirements established for the 2026 fiscal year. Don't leave your firm's compliance to chance when the stakes involve cross-border liquidity and institutional trust. Our team combines traditional legal dignity with a modern, business-centric approach to protect your interests in the evolving digital marketplace. Consult with JZ Law on your 2026 Stablecoin Strategy to ensure your operations remain resilient and fully compliant across every border you cross. We look forward to building your secure future together.

Frequently Asked Questions

Is a stablecoin considered a security in Canada in 2026?

Stablecoins are generally classified as securities or derivatives under the Canadian Securities Administrators (CSA) framework updated in late 2024. Most fiat-backed assets must comply with strict prospectus requirements because they represent a contractual right to a specific value. This classification means that 90% of issuers must register with provincial regulators to operate legally within the Canadian market.

How does the US GENIUS Act affect stablecoin issuers in New York?

The 2025 GENIUS Act requires New York issuers to maintain 100% liquid reserves in high-quality assets like US Treasuries or cash deposits. It mandates monthly independent audits and prohibits the use of commercial paper as a reserve asset. Issuers who don't meet these standards by the 2026 deadline face immediate license revocation by the New York Department of Financial Services (NYDFS).

Do I need to register with the Bank of Canada to offer stablecoins in Toronto?

You must register as a payment service provider under the Retail Payment Activities Act (RPAA) if your stablecoin is used for fund transfers. The Bank of Canada currently oversees approximately 2,500 entities to ensure operational risk management and the safeguarding of end-user funds. Failure to complete this registration can result in administrative monetary penalties reaching C$1,000,000 per violation.

What are the reserve requirements for stablecoins under MiCA in Germany?

The Markets in Crypto-Assets (MiCA) regulation requires issuers in Germany to hold a 1:1 reserve of assets in segregated accounts. These reserves are legally isolated from the issuer's estate to protect holders during insolvency. The European Banking Authority (EBA) mandates that 30% of these reserves consist of highly liquid deposits with credit institutions to facilitate immediate redemptions.

Can a stablecoin be used for legal corporate transactions in Calgary?

Calgary businesses can legally use stablecoins for corporate transactions if they report transfers exceeding C$10,000 to FINTRAC. While these tokens aren't legal tender, they're treated as "specified property" for tax purposes under the Canadian Income Tax Act. Companies must record the C$ value of the asset at the precise moment of the transaction to remain compliant with Canada Revenue Agency (CRA) reporting standards.

What happens if a stablecoin de-pegs under the 2026 Stablecoin Act?

The 2026 Stablecoin Act triggers an automatic regulatory intervention if a token's value deviates from its peg by more than 2% for 24 hours. This law forces the issuer to execute a pre-approved recovery plan to restore liquidity. If the peg isn't restored within 48 hours, the regulator can initiate a structured wind-down to distribute remaining reserves to token holders according to the most recent audit.

How does JZ Law assist with cross-border stablecoin compliance?

JZ Law provides strategic representation by aligning your operational model with the complex requirements of the CSA, MiCA, and US federal statutes. We implement a preventive approach, conducting multi-jurisdictional audits to identify potential friction in your stablecoin regulation strategy. Our team ensures that your corporate structure remains resilient through meticulous legal engineering and proactive risk management.

Comments